I. Signals of a Global Market Reshuffle

The global copper scrap trade is entering a new cycle of restructuring. Over the past decade, the global trade network for copper scrap has been highly dependent on China, forming a circular model of “raw material export – Chinese smelting – product re-export.” However, since China implemented the Solid Waste Import Ban in 2018, the global supply chain has been forced to reorganize, and a large volume of copper scrap has been redirected to Southeast Asian countries.

By 2020, as Southeast Asian countries gradually tightened import controls, the global copper scrap market ongoing a “second phase of flow rebalancing.” According to publicly available information, global copper scrap trade volume reached approximately 6 million metric tons in 2024. China remains the largest importer of copper scrap, accounting for around 40% of global imports. The United States and the European Union are the main exporters, but their export destinations have become increasingly diversified, indicating a clear pattern of regional redistribution. The global copper scrap trade network is thus undergoing a fundamental structural reshaping.

II. China’s Policy Shift and Global Implications

China

Throughout the evolution of global copper scrap trade, policy has always been the central factor shaping trade flows. Over the past decade, China’s regulatory transformation has effectively marked the beginning of the global copper scrap market’s restructuring. For years, China was the world’s largest importer of copper scrap, accounting for roughly 40% of global trade volumes. At that time, China allowed the import of certain solid wastes (including used wires, motors, electronic parts, and plastics) under the category of “recyclable resources,” to be processed domestically. This model contributed significantly to resource recovery and raw material supply but also caused serious environmental pollution and regulatory disorder.

In 2018, China officially launched its Solid Waste Import Ban, initially prohibiting 24 categories of solid waste, later expanding the scope, and by 2021, banning all forms of solid waste imports. Within this framework, copper scrap became a special case. Through the GB/T 38471-2019 “Recycled Copper Raw Materials” national standard, China reclassified high-purity, low-impurity copper scrap as “recyclable raw material” instead of “solid waste.” This shift transformed the import system from “easy customs clearance” to “quality-first control.”

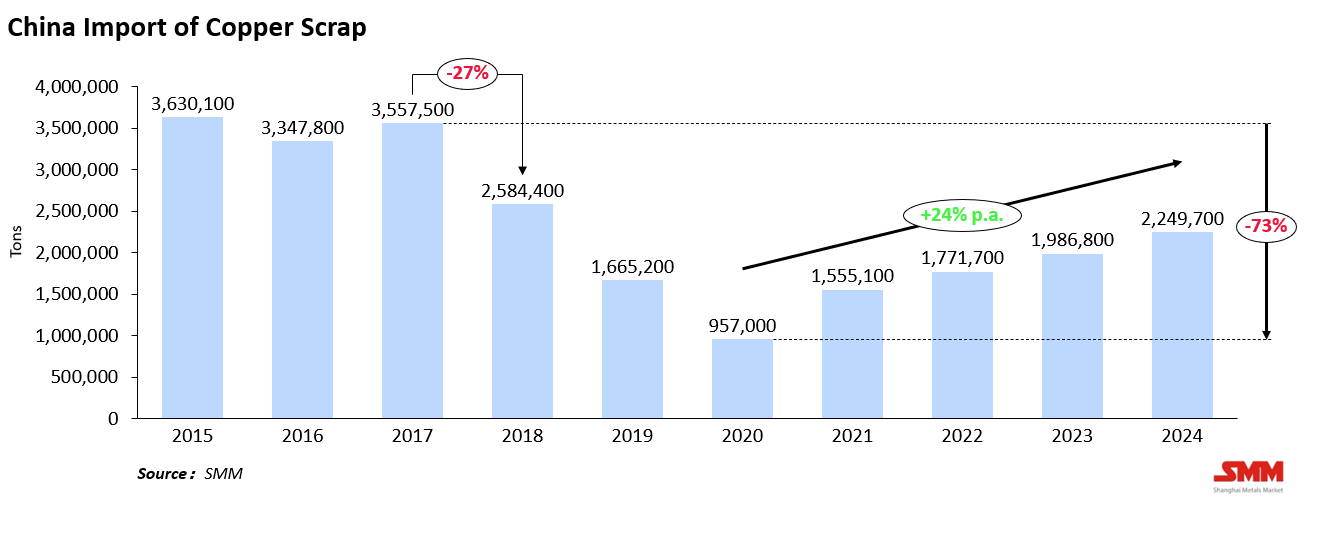

The impact was immediate: low-quality copper scrap was effectively blocked, and large volumes of U.S. and European copper scrap were diverted elsewhere. Data clearly reflects this policy effect — China’s copper scrap imports fell from 3.55 million tons in 2017 to 2.58 million tons in 2018, a 27% drop, and further declined to 0.95 million tons by 2020, down 73% from the 2017 peak. Although imports gradually recovered to 2.25 million tons in 2024, they remain far below historical highs. China’s high-standard policy framework in 2018 directly triggered the first wave of global copper scrap trade restructuring.

Southeast Asia

After China tightened its import controls, Southeast Asia temporarily became the world’s main “alternative receiving region” for copper scrap. Countries such as Malaysia, Vietnam, Thailand, and Indonesia, leveraging their proximity and more lenient customs procedures, quickly absorbed the trade volume diverted from China.

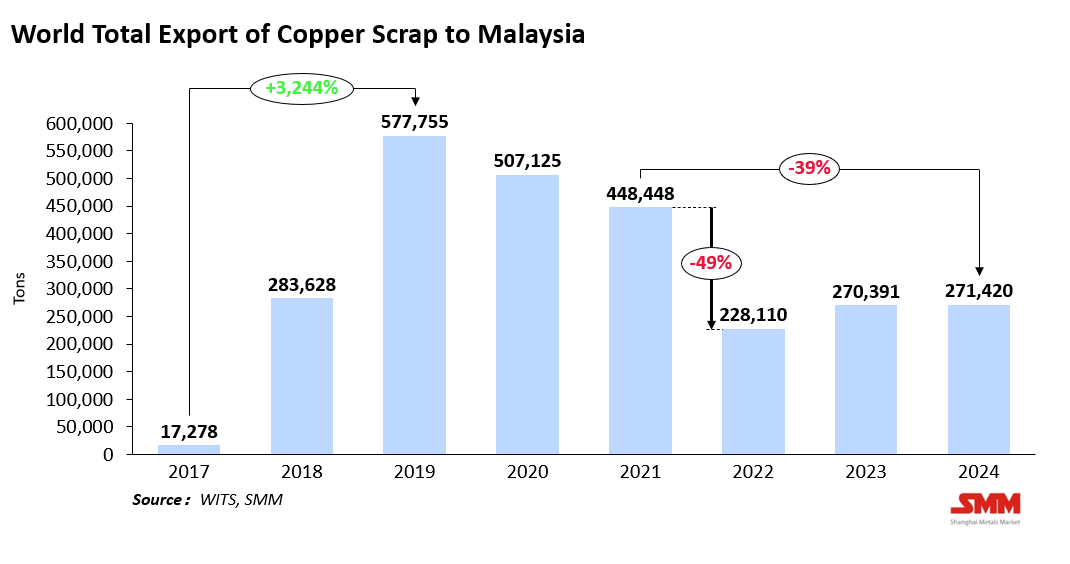

For example, Malaysia’s copper scrap imports surged from 17,000 tons in 2017 to a peak of 570,000 tons in 2019, before declining to 448,000 tons in 2021. This rapid expansion, however, led to environmental pollution, smuggling, and non-compliant processing, prompting these countries to strengthen regulations:

- Malaysia introduced the SIRIM certification system in 2021, requiring copper scrap imports to contain at least 94.75% copper and limiting impurity levels, while enhancing port inspection and traceability, significantly extending customs clearance times.

- Vietnam enacted a new Environmental Protection Law in 2020, imposing stricter purity standards and a quota-based import management system.

- Thailand amended its Ministry of Environment regulation in 2023, reinforcing import licensing and source declaration, and explicitly banning mixed scrap imports.

These measures have transformed Southeast Asia from a “transit hub” for copper scrap into a region with higher environmental and regulatory standards. The effects were evident in import data — in Malaysia, total copper scrap imports dropped from 448,000 tons in 2021 to 228,000 tons in 2022, a 49% year-on-year decline, and only modestly recovered to 270,000 tons by 2024, still 39% below pre-regulation peaks. As a result, many traders have shifted their supply chains toward India and the Middle East, marking the beginning of the second rebalancing of global trade flows.

Europe and the United States

Meanwhile, Western economies have moved toward dual-end control of both exports and production of copper scrap. In the European Union, the Basel Convention and the Carbon Border Adjustment Mechanism (CBAM) have become the core policy pillars — restricting exports of low-grade scrap and integrating carbon emissions into trade requirements. The goal is to prevent pollution leakage while encouraging closed-loop recycling within the EU. In the United States, the Institute of Scrap Recycling Industries (ISRI) continues to promote export standardization, while legislation and tax incentives have been introduced to boost domestic recycling and reduce reliance on overseas reprocessing.

Overall, the world’s major copper scrap importers and exporters are shifting from “open access” to “high-standard and environmentally constrained” trade models. While this raises trade friction and reduces efficiency, it also accelerates the sector’s evolution toward quality, transparency, and sustainability.

III. Restructuring Trade Flows: The Rise of New Hubs

Policy evolution has not only changed the direction of copper scrap flows but has also driven companies to restructure their supply chains and capacity distribution. In recent years, the global copper scrap market has evolved from “Southeast Asian transit” to “multi-regional rebalancing.”

Phase I (2018–2020): Southeast Asia as China’s Substitute Transit Zone After China’s import ban, massive volumes of copper scrap from the U.S., Europe, and Japan were rerouted to Southeast Asia. Malaysia, Vietnam, and Thailand became key transit and light-processing centers, where copper scrap entered under the label of “recyclable resources,” underwent basic sorting or melting, and was then re-exported to China for smelting.

Phase II (2021–2024): Tightened Regulation and Diversified Flows As environmental and compliance challenges surfaced, Southeast Asian nations introduced stricter import controls, leading to flow diversification. India and the Middle East emerged as new receiving centers — India with its robust smelting base and growing downstream demand, and the UAE with free-port policies that attracted numerous recycling plants. Other players such as Turkey, Saudi Arabia, and South Korea are also expanding recycling capacity and becoming integral to the new global flow network.

Phase III (2025 onward): The Era of Multi-Polar Trade The copper scrap trade is now entering a new phase of structural realignment. With rapid expansion of recycling capacity in India, the UAE, and South Korea, emerging markets are building comprehensive smelting and refining systems. Global copper scrap trade is transitioning from dependence on a single dominant market to a multi-center system, led by nations with policy and production advantages. According to SMM, from 2015 to 2024, copper scrap imports into India and the Middle East grew steadily — India’s imports rose from 175,000 tons in 2015 to 330,000 tons in 2024.

IV. Geopolitical and Future Dynamics

The global copper scrap trade is shifting from being price-driven to being shaped primarily by politics and compliance. International trade policy, green standards, and geopolitical friction are collectively redefining the cost and structure of cross-border flows.

The prolonged U.S.–China trade tensions have disrupted traditional trade chains. To avoid tariff barriers and origin-based restrictions, some materials are rerouted through Southeast Asia or Mexico, forming increasingly complex supply networks. However, this “circuitous trade” faces growing risks as customs scrutiny and origin verification intensify, extending clearance times and raising costs.

Simultaneously, the EU’s CBAM is exerting profound influence on the global metals supply chain. For Asian recyclers and smelters, low-carbon production, green certification, and traceability have become essential requirements for maintaining access to European markets. In response, Southeast Asian nations are accelerating the development of green smelting ecosystems, a move that drives industrial upgrading but also raises compliance costs.

Looking ahead, Southeast Asia’s role as the world’s primary re-export and reprocessing center for copper scrap is expected to diminish. While environmental regulation and import scrutiny will suppress low-end operations, India and the Middle East are poised to become new hubs, leveraging cost advantages, port infrastructure, and open investment policies.

In summary, under the combined forces of environmental policy, trade barriers, and geopolitical shifts, global copper scrap trade will evolve toward greener and more localized supply chains. SMM estimates that by 2030, cross-border copper scrap trade costs will rise by about 15% from current levels, while industry profits will increasingly shift from traditional traders to integrated smelting and compliance-oriented enterprises.

V. Copper Scrap: From Waste to Strategic Resource

In the past decade, trade patterns were shaped largely by policy and geopolitical shifts. Today, however, the restructuring of copper scrap flows represents not just a trade realignment, but a systemic industrial transformation.

The convergence of geopolitical tensions, environmental compliance, and carbon standards is collectively forging a new global copper scrap order. Policy focus has moved from “restriction and access” toward “certification and traceability,” while enterprises are shifting from “export orientation” to “local recycling and green smelting.”

As countries pursue resource self-sufficiency and circular economy strategies, the value of copper itself is being redefined — copper scrap is no longer mere recoverable waste, but a strategic material essential to energy transition and manufacturing resilience.

It is foreseeable that the global copper scrap market will continue to evolve toward greater transparency, standardization, and sustainability. Those who can establish compliant, low-carbon, and traceable systems first will secure a decisive advantage in the next phase of the global copper competition.